[ad_1]

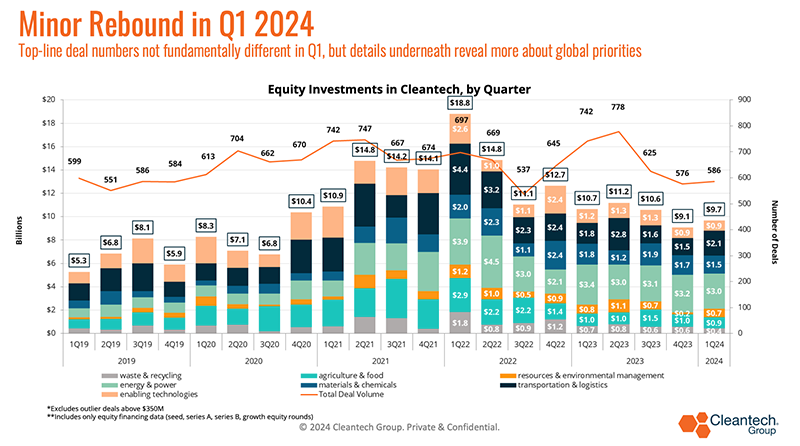

In Q1 of 2024, we noticed extra of the “new regular” in enterprise & progress investing – following the explosive years of financing throughout the pandemic, fairness financing ranges have basically leveled out however have settled at common ranges larger than the averages pre-pandemic.

Some issues that have been distinctive to Q1:

- Vital exercise within the hard-to-abate sectors, e.g., metal and cement (extra on these later) – these have been the industries historically thought-about most troublesome to decarbonize and the applied sciences most dangerous to again financially, however they’ve seen constantly robust funding quarters.

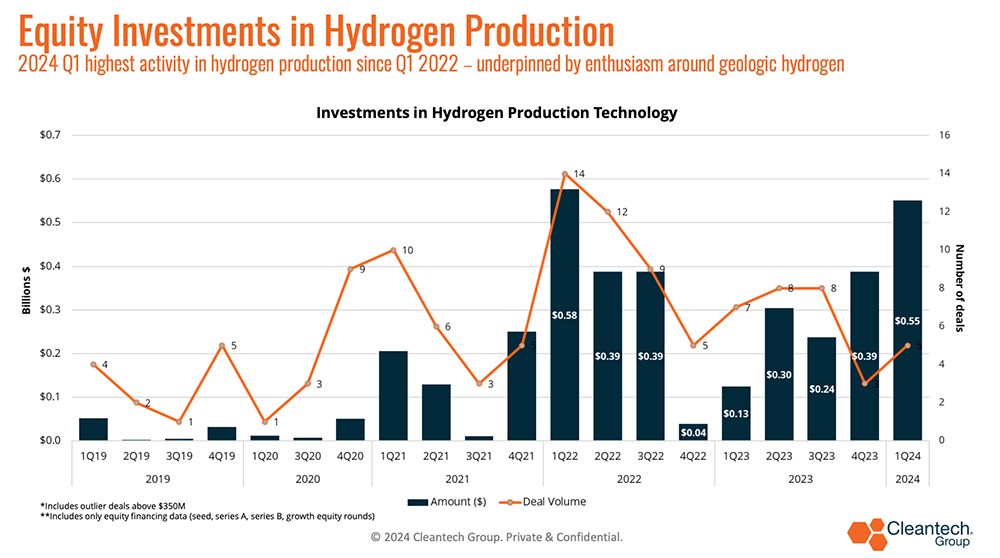

- Regardless of among the lingering doubts round transitions to hydrogen, hydrogen manufacturing applied sciences noticed a really robust enterprise quarter – underpinned largely by enthusiasm over new geologic hydrogen exploration applied sciences.

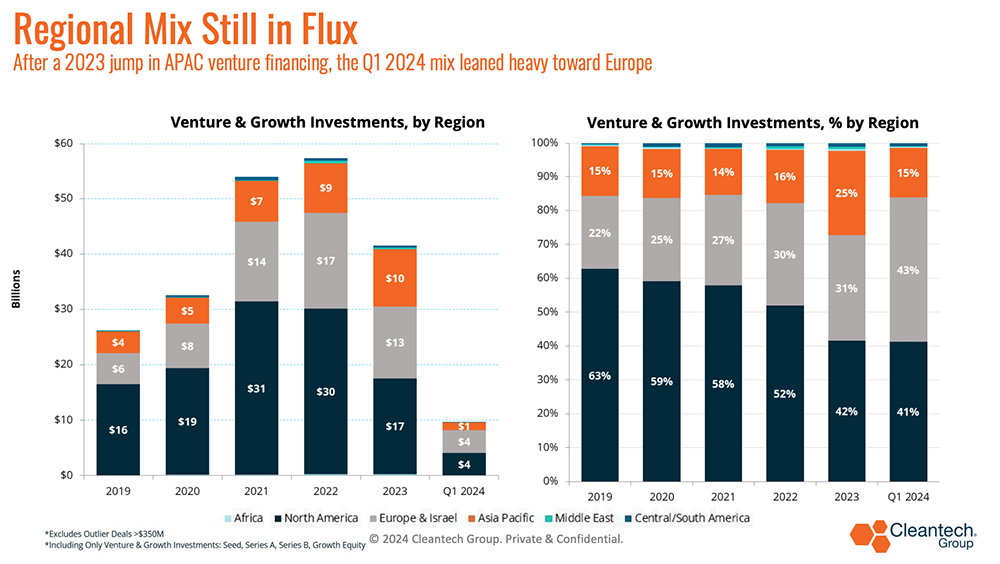

- One other quarter of a “cooling” in Asia-Pacific (continued from Q1 2023) versus the very important bounce, particularly in Power & Energy financing in most of 2023 – the combination shifted closely European in Q1 with the Europe progress case principally coming from Transportation & Logistics tech (see beneath).

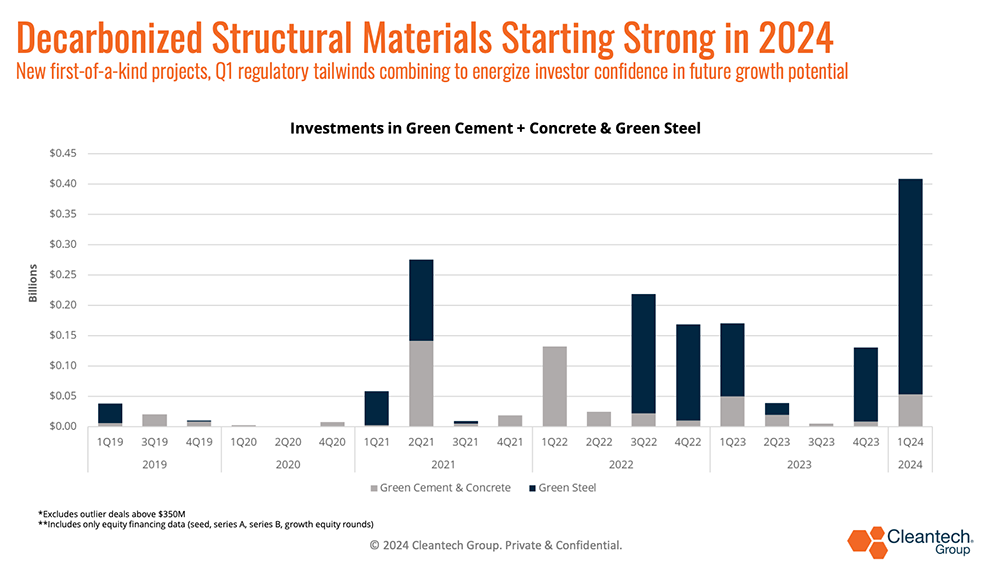

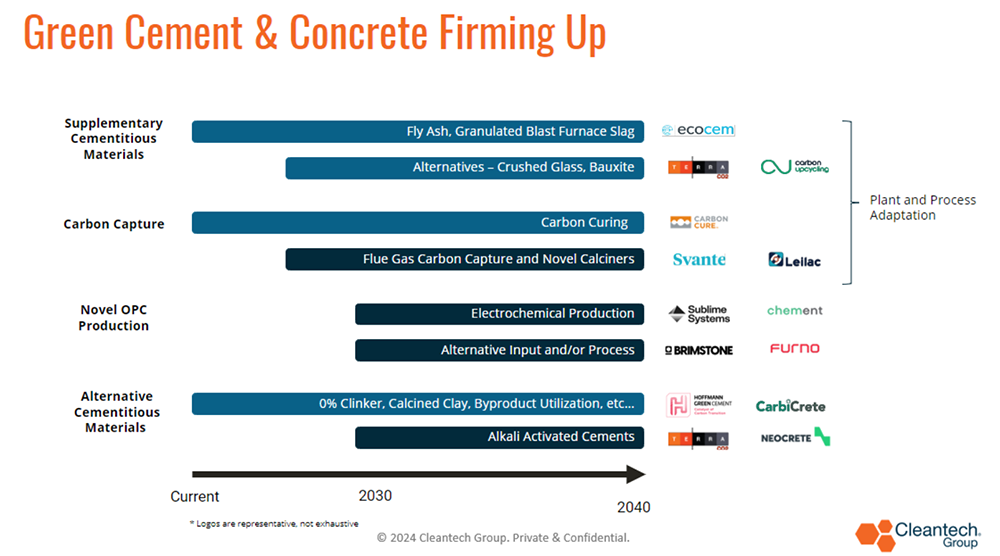

Cement and Concrete Headline Q1

The early exercise in inexperienced metal and inexperienced cement and concrete is among the headline tales of this primary quarter. These historically hard-to-abate sectors now have sufficient of a slate of modern options to start out charting a path ahead to decarbonization.

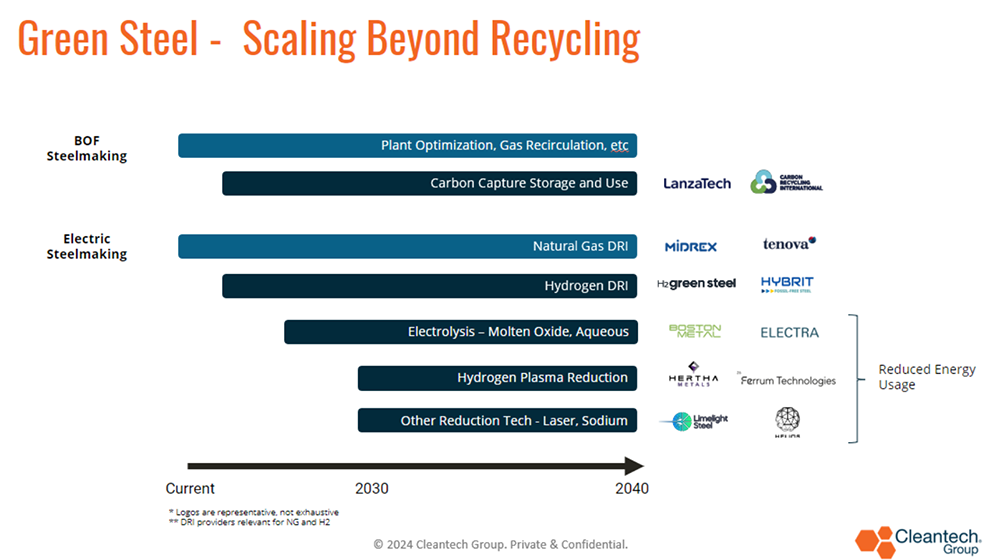

We at the moment are at an attention-grabbing stage during which there are new inexperienced metal and cement manufacturing applied sciences which are getting into the market (principally via demonstration vegetation, however some at industrial scale) – a primary “tranche” of applied sciences is rising whereas the extra nascent applied sciences are seeing extra enterprise help (see diagrams beneath for our tackle the “tranches” of inexperienced metal and inexperienced cement improvement):

Some key offers in these areas from Q1 2024:

The Biden Administration just lately introduced $6B for 33 undertakings in hard-to-abate sectors, some modern options benefitting immediately embrace:

- Deeply Decarbonized Cement (as much as $189M) by Brimstone

- First Business Electrochemical Cement Manufacturing (as much as $86.9M) by Chic Programs

- Steam-Producing Warmth Pumps for Cross-Sector Deep Decarbonization ($as much as $145M) by Skyven

Hydrogen Additionally Reveals Funding

Maybe not surprising, per se, however actually the hopes round potential for geologic hydrogen turned extra palpable this previous quarter. See the chart beneath, the place Q1 was probably the most important when it comes to fairness financing towards hydrogen manufacturing expertise – the over half a billion {dollars} spent consisted of funding in a number of hydrogen manufacturing pathways, however was considerably underpinned by a $245M Sequence B spherical invested in white hydrogen firm Koloma days after Koloma additionally acquired a $900K grant from the U.S. Division of Power, and fewer than a yr off a $91M Sequence A spherical.

The passion round geologic hydrogen (hydrogen that happens naturally in underground reservoirs) is two-fold:

1) It’s hydrogen that’s extracted and never produced via a thermal or electrical course of

2) Consequently, it avoids carbon emissions from manufacturing processes.

Accessing geologic hydrogen in a low-cost method would cut back the necessity to construct out new renewables to provide inexperienced hydrogen and, in concept, commerce electrical energy price for price of compression, transport, and storage of hydrogen.

Trying In the direction of Q2

- Business traction and offtake agreements would be the KPI for firms hoping to exit the fairness financing continuum out to bankability. This can be an apparent assertion, however firms which are capable of finding inventive methods to entry pockets of willingness-to-pay are going to start a journey to decrease price of capital before their opponents.

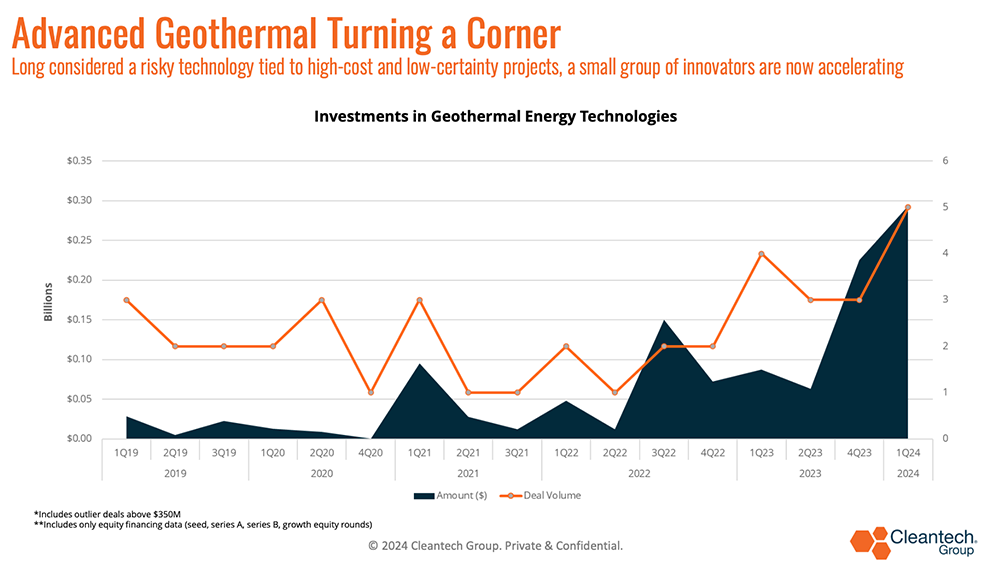

- An area to observe is enhanced geothermal – regardless of having important potential to supply 24/7 agency clear energy, difficult undertaking economics have remained a barrier. New applied sciences in drilling and closed-loop programs have proven promise to higher entry the latent energy potential in scorching, dry rock geothermal deposits.

- This previous quarter was probably the most important in geothermal enterprise financing since we started monitoring the area, some key offers included:

- Quaise: $21M Sequence A for provide chain improvement, subject operations to advance deep geothermal drilling

- Fervo: $244M to additional operations at Cape Station to help clear electrical energy to the grid by 2026. Fervo has a number of energy buy agreements, together with with Google and East Bay Group Power

- Sage Geosystems: $17M Sequence A to help 3MW website in Texas after efficiently finishing full-scale industrial pilot that produced 200kw for greater than 18 hours and 1 MW for half-hour

How Can Local weather Innovation Proceed to Evolve?

How Can Local weather Innovation Proceed to Evolve?

- It’s all about attacking the associated fee curve: so lots of the modern applied sciences that we’ve adopted for years at the moment are getting into actual initiatives and manufacturing. As soon as market forces kick in and demand pull is noticed, you’ll have extra entrants and start the financial journey to commoditization – getting previous inexperienced premiums and towards affordability might be important for batteries, hydrogen manufacturing, and low-carbon industrial merchandise (metal, cement, chemical compounds).

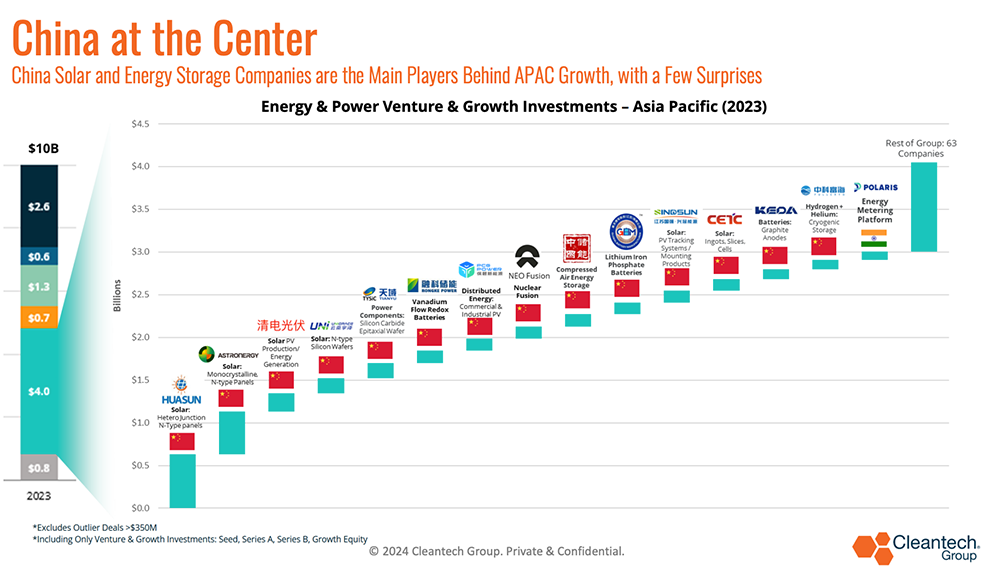

- There’s a behavior of referring to China on this regard as a siloed case for particular applied sciences – however finally China is a proxy for the associated fee pressures that innovators must sustain with as soon as scale manufacturing is on-line (a change from the R&D part when tech efficiency metrics are usually extra central considerations).

- See the graphic beneath, the place China was the central innovation & enterprise financing for vitality in APAC in 2025 – if that is any indication, one can count on to see related ranges of competitors outdoors of simply photo voltaic and batteries, however in all features of vitality applied sciences.

Some offers this previous quarter that help vitality applied sciences getting into industrial phases embrace:

- Antora Power raises $150M for thermal vitality storage to help commercialization and a producing facility in San Jose, California

- NineDot Power raises $225M from Carlyle Group and Manulife Funding

- Ascend Components raised a contemporary $162M Progress Fairness spherical to finalize North America’s first recycled cathode from black mass manufacturing facility

- Lohum raised a $54M Sequence B to develop their operations in EV battery-to-energy storage programs conversion whereas getting into the recycled cathode supplies market

Chinese language Affect on the Way forward for the EV Market

The subsidies to Chinese language EV producers, as well-documented in current stories, may be very important and has allowed for a fast scaling of EV manufacturing and gross sales (each inside China and Chinese language-produced autos for export).

There may be already a excessive 27.5% import tariff on Chinese language-built autos within the U.S., so the onus will now be on U.S. producers to slash prices via studying results and use of expertise.

- A important problem might be that Chinese language producers are already producing at important scale (close to 10M EVs bought by Chinese language producers final yr vs. 1.2M within the U.S.). Subsidies or not, the educational results from mass manufacturing are to not be understated – that is the place producers resolve manufacturing inefficiencies (e.g., cut back scrap), optimize manufacturing facility layouts and operations administration programs, acquire negotiating energy with suppliers, and customarily obtain economies of scale (i.e., spreading CAPEX of amenities throughout extra income).

- Passenger EVs are usually the main target of this dialog, however buses and fleet autos are a frontier market that may even be important – the educational results gained by Chinese language scale manufacturing might already be paying dividends in these markets (Automotive World, Proterra Might Not be a Bellwether for e-bus Failure within the U.S.).

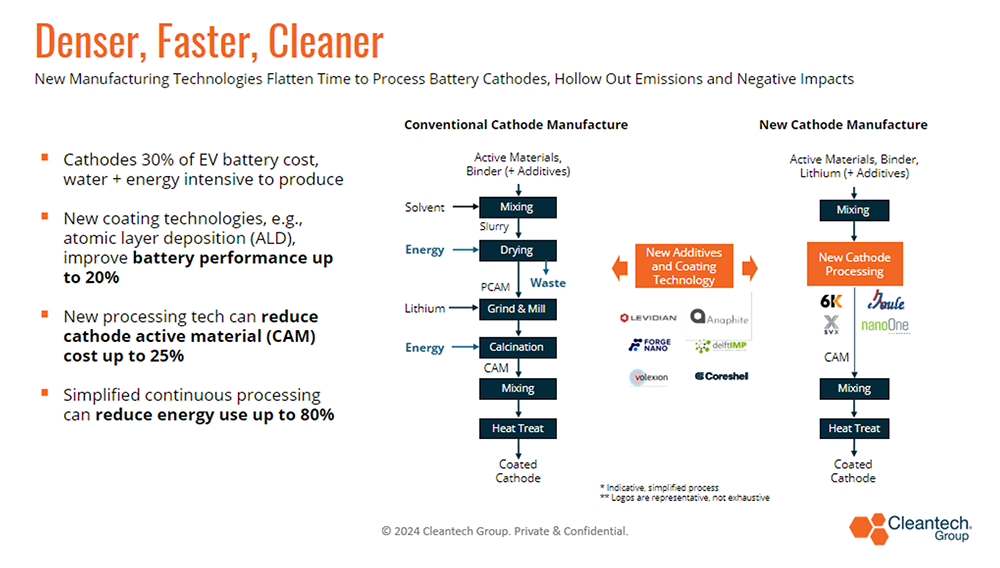

- Leveraging new expertise is among the greatest methods U.S. and Western EV producers can begin decreasing prices to compete higher globally. There are numerous variables to contemplate in price discount, however our speculation at Cleantech Group is that innovation will cut back prices of cathodes in batteries – batteries can comprise as much as 40% of auto price and cathodes 30% of that battery price. Some improvements that we’re keeping track of beneath:

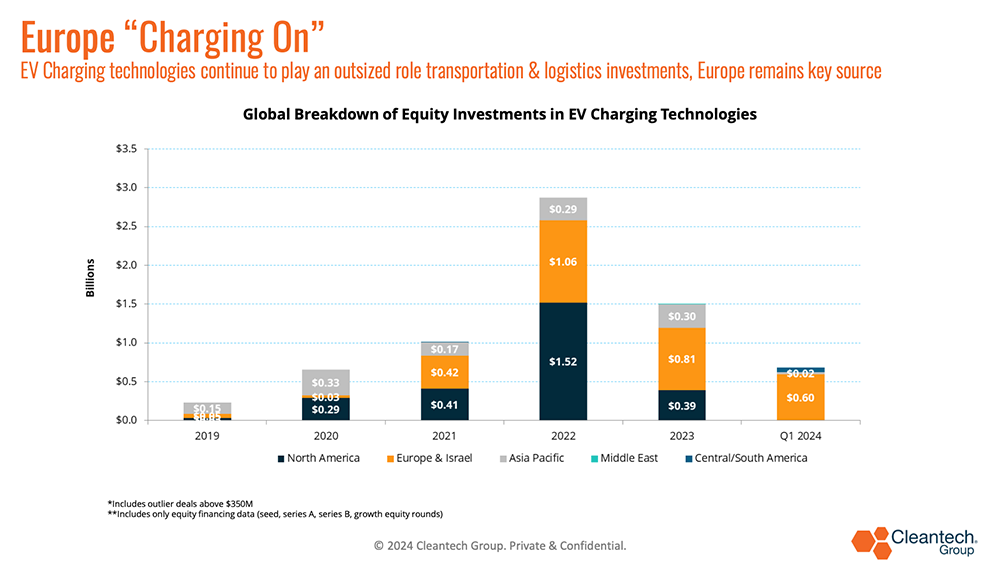

Europe Stays Key Supply

An attention-grabbing pull-through impact of world EV rollout has been the alternatives it’s creating for innovation and progress of recent applied sciences in EV charging – Europe has seen constant enterprise exercise on this regard over the previous few years (see chart beneath).

Some dynamics making the state of affairs in Europe distinctive:

- Coverage indicators on the EU degree:

- 2035 ICE ban for brand spanking new vehicles authorized in 2023

- Deal on decarbonization of industrial quality autos agreed in February, with bold targets

- Deal on charging infrastructure in 2023 (AFIR)

- Offers on the Batteries Regulation and Vital Uncooked Supplies Act – the EU’s legislative framework round EVs was basically accomplished during the last 18 months and covers the entire worth chain

- The EU has a lot decrease tariffs on Chinese language EVs than the U.S. does, at a time when China has main overcapacity. Therefore, competitively priced Chinese language EVs are flooding into Europe and placing downward stress on the costs of non-Chinese language EVs

- Europe has had one single charging customary for some time, in contrast to the U.S. the place there have been a number of till Tesla’s just lately received out

[ad_2]